Company Overview

![]() Tootsie Roll Industries (NYSE: TR) and its subsidiaries manufacture and sell confectionery products in 75 countries worldwide. Tootsie Roll’s brand portfolio is composed of many well known products, such as Tootsie Rolls, Tootsie Pops, Junior Mints, Charleston Chews, and Andes mints.

Tootsie Roll Industries (NYSE: TR) and its subsidiaries manufacture and sell confectionery products in 75 countries worldwide. Tootsie Roll’s brand portfolio is composed of many well known products, such as Tootsie Rolls, Tootsie Pops, Junior Mints, Charleston Chews, and Andes mints.

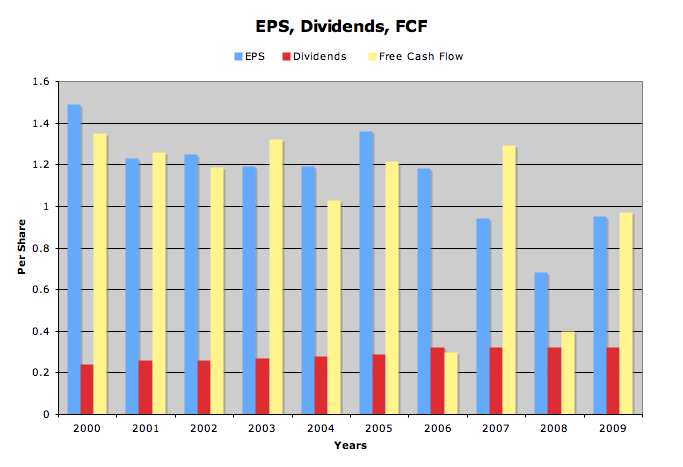

EPS, Dividends, FCF

| Annual Growth Rates | Earnings Per Share | Dividends Per Share | FCF Per Share |

|---|---|---|---|

| 10 year | (4.83%) | 3.22% | (3.56%) |

| 5 year | (8.58%) | 2.49% | (5.46%) |

| 1 year | 39.71% | 0% | 143.12% |

Expected Earnings

- FY 2011 – 0.89

In the just released earnings statement, eps for 2010 was 0.94

TR has been on a declining trend for most of the past decade. A small part of this can be attributable to dilution of shares, as TR usually awards shareholders a 3% stock dividend every year. This has increased shares outstanding from 50 million to 57 million over the past decade. The effect of this would be minor at best. What is truly concerning is the sluggish revenue growth and rapidly declining margins.

A 10 year average dividend growth of just 3.2% barely covers inflation (using the oft-cited average of about 3% a year). Though dividends have not been cut during this time, there have been numerous years of no increase. The current dividend of .32 a share has been stagnant since 2006.

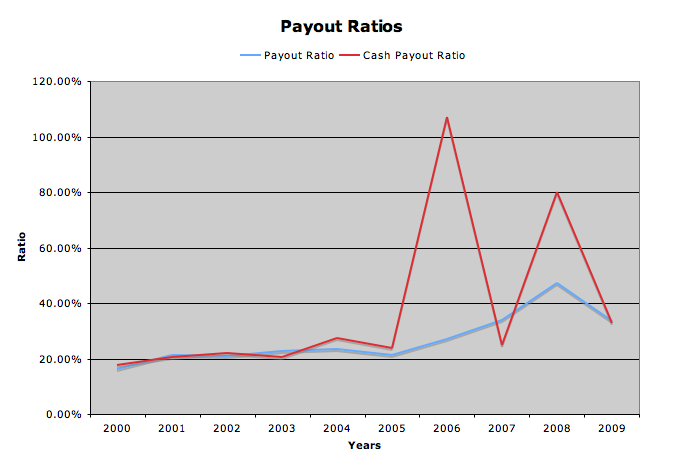

Payout ratios are both at acceptable levels, and leave plenty of room for growth.

Revenue and Margins

| Years | Revenue (in thousands) |

|---|---|

| 2000 | 427,054 |

| 2001 | 391,755 |

| 2002 | 393,185 |

| 2003 | 392,656 |

| 2004 | 420,110 |

| 2005 | 491,084 |

| 2006 | 501,140 |

| 2007 | 497,717 |

| 2008 | 496,016 |

| 2009 | 499,331 |

10 year growth average is 1.73%. Reported revenue for 2010 is 517,149 thousand, a one year increase of 3.6%.

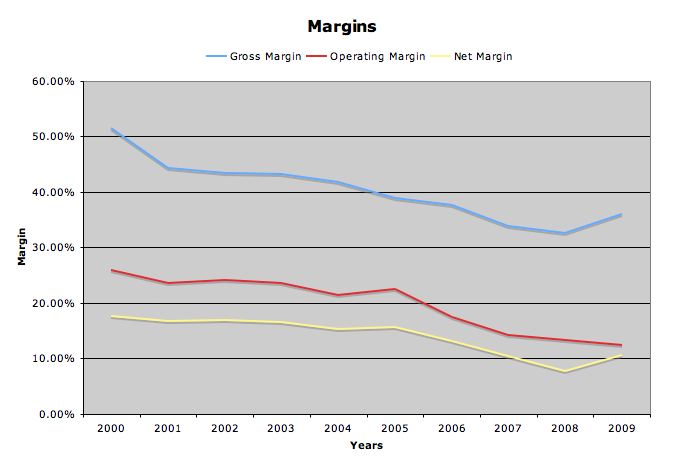

Margins have been steadily decreasing for years. Reduction in gross margin could be an effect of rising commodity prices, which have been at historically high levels for the past few years. This includes sugar and cocoa prices. And while some commodities have seen prices decrease, such as dairy, they have not been sufficient to offset the higher cost of others.

The corresponding decreases in both operating and net margins shows TR cannot control costs. For example, though revenue has barely budget in a decade, selling, administrative and marketing costs have gone from 70 million in 2000 to 105 million in 2009.

Balance Sheet

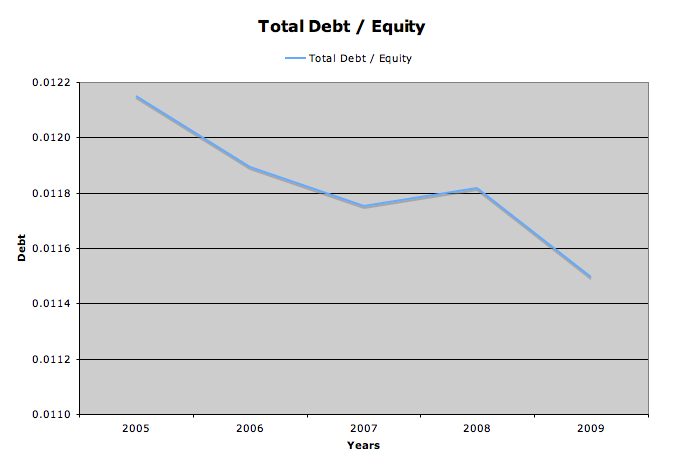

The balance sheet is one area TR is very strong. Incredibly low debt levels are usually a good sign, although in this situation, a little debt may not be a bad thing, if it allows TR to increase it’s sales, earnings, or dividends.

Current ratio is 3.8, and debt is 1.14% of capital structure. Like Hershey, Tootsie Roll Ind. has a fair amount of intangibles and goodwill on it’s balance sheet, amounting to 248 million, or 30% of total assets.

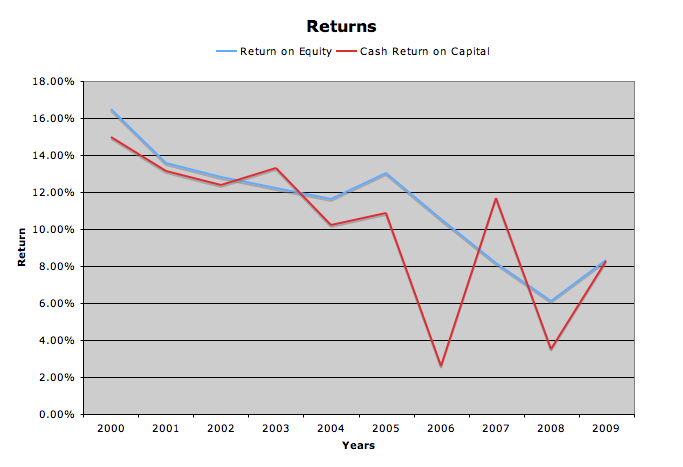

Returns

Returns have also been on a steady decline over the years, another bad sign.

Stock Price Valuations

current price – 28.17

5 year low p/e – 23

p/e (ttm) – 29.97

p/e (forward) – 31.7

peg – N/A

p/tangible book – 3.9

5 year high dividend yield – 1.4%

dividend yield – 1.14%

Conclusion

It seems the only thing enticing about Tootsie Roll Industries are their snacks, not their business.

For comparison, see my analysis of The Hershey Company

To get all my updates, please subscribe to my rss feed

Full Disclosure: I do not own any TR. My Current Portfolio Holdings can be seen here

1 Comment

Very interesting! This has never been on my radar, and based on your analysis, I won’t get in anytime soon!

You nailed it – only thing enticing about Tootsie Roll Industries are their snacks, not their business!