Many investors don’t think of mining stocks as dividend growth companies, because of their lower dividend yields. The Canadian mining sector has largely been overlooked by the Canadian dividend investing crowd. Yet these are “dividend growth” companies with strong balance sheets. They have recently raised their dividends, and have more potential for share price increase. Take PotashCorp (POT) as an example, which recently raised its dividend by a whopping 33%. By avoiding the lower-yield mining companies, many investors may be giving up a “golden” opportunity for future growth, when the resource sector rebounds.

Many investors don’t think of mining stocks as dividend growth companies, because of their lower dividend yields. The Canadian mining sector has largely been overlooked by the Canadian dividend investing crowd. Yet these are “dividend growth” companies with strong balance sheets. They have recently raised their dividends, and have more potential for share price increase. Take PotashCorp (POT) as an example, which recently raised its dividend by a whopping 33%. By avoiding the lower-yield mining companies, many investors may be giving up a “golden” opportunity for future growth, when the resource sector rebounds.

The Canadian mining sector also has companies which are trading at their two and three year lows. In a rising market where many stalwart blue-chips are trading at their 52 week highs, there may indeed be opportunity in this beaten up sector. This is a sector that has been on my watch list for a few months, and I am ready to make a move. These aren’t penny-stocks, or junior mining companies, but giant multi-billion dollar companies with global reach. The majority of these Canadian mining companies are also “interlisted” on the NYSE as well as the TSX.

Three Canadian mining companies are now on my watch list: Goldcorp Inc. (G), Teck Resources (TCK), and Potash Corp. (POT). I’ve also included Barrick Gold (ABX) and Agrium (AGU) for comparative purposes. As discussed in the conclusion, Barrick is now off my watch list. Table-1 below gives the basic fundamentals and dividend info.

| Company | Ticker (NYSE) | Market Cap. | Share Price | Div. Yield | Payout Ratio | Profit Margin | Debt to Equity |

| Agrium | AGU | 16.1 B | 99.89 | 2.00% | 24.8% | 8.95% | 57.24% |

| Barrick Gold Corp. | ABX | 32.1 B | 31.26 | 2.55% | -124.0% | -4.57% | 56.89% |

| Goldcorp Inc. | GG | 27.9 B | 33.52 | 1.79% | 28.8% | 32.18% | 3.42% |

| Potash Corp. | POT | 34.4 B | 38.93 | 2.87% | 42.9% | 27.97% | 41.17% |

| Teck Resources | TCK | 18.4 B | 30.60 | 2.86% | 40.5% | 7.84% | 40.02% |

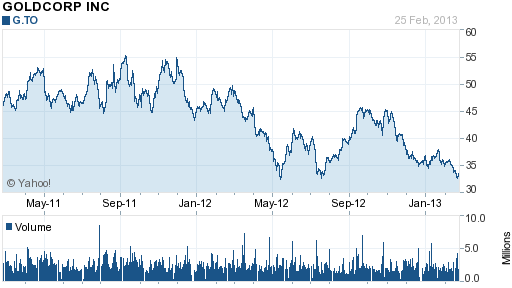

GG – Goldcorp Inc.

Goldcorp (GG) is the world’s second largest Gold producer, in terms of market cap, and is worth over 28 billion dollars. In terms of productions tonnes, it is the world’s fourth largest, with an annual output of 71 production tonnes in 2011 (see Wikipedia). Goldcorp has the lowest dividend yield of the five Canadian mining stocks I first perused, with a dividend yield of only 1.78%.

However Goldcorp has a phenomenal balance sheet, with a debt-to-equity ratio of only 3.4%. This is a low debt level for any company, and Goldcorp has continually shown itself to be a well run and managed company. Goldcorp also has a high profit margin at 32.1%, and low dividend payout ratio (DPR) of only 28.8%. This is a great combination. So there is more than enough room to grow the dividend. Goldcorp also has the benefit of being a monthly dividend payer. Goldcorp would have made the top of my list, if it were not for the lower yield. Goldcorp is “interlisted” on both the TSX as G, and the NYSE as GG. The company is also trading near its three year lows.