Company Overview

Walmart (NYSE: WMT) is the world’s largest retailer. Wmt serves customers and members more than 200 million times per week at more than 8,613 retail units under 55 different banners in 15 countries, and employs 2 million people worldwide.

Walmart (NYSE: WMT) is the world’s largest retailer. Wmt serves customers and members more than 200 million times per week at more than 8,613 retail units under 55 different banners in 15 countries, and employs 2 million people worldwide.

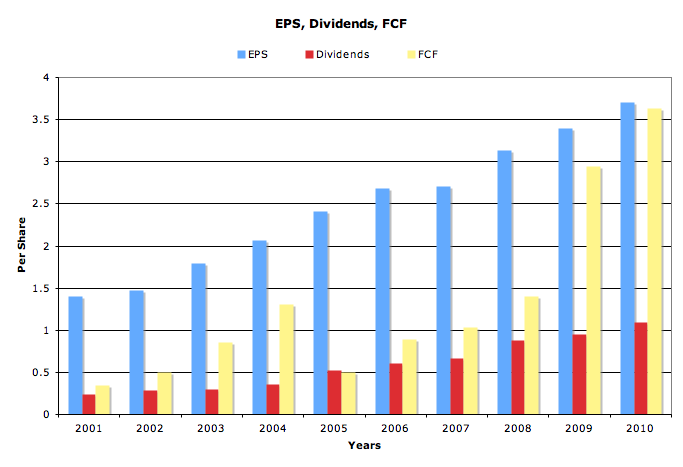

EPS, Dividends, FCF

Expected Earnings

- 2011 – 4.05

- 2012 – 4.45

Expected Dividends (based on 5 year growth rate)

- 2011 – 1.40

- 2012 – 1.62

Free Cash Flow

- FCF per diluted share has grown by an average of 29.4% over the past 10 years

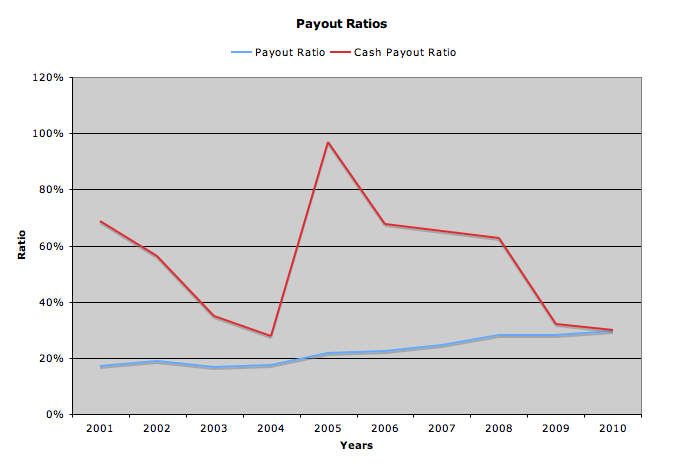

Even though I graph both payout ratios based on earnings and free cash flow, I generally consider fcf to be the more important metric. As shown, wmt’s payout ratio based on earnings has been climbing, but still sits under 30%. The cash payout ratio however, has seen some years of near 100% payout, namely 2005. Since then it has been lowered considerably, and as of fy 2010 the dividend was only 30.05% of fcf, leaving plenty of room for growth.

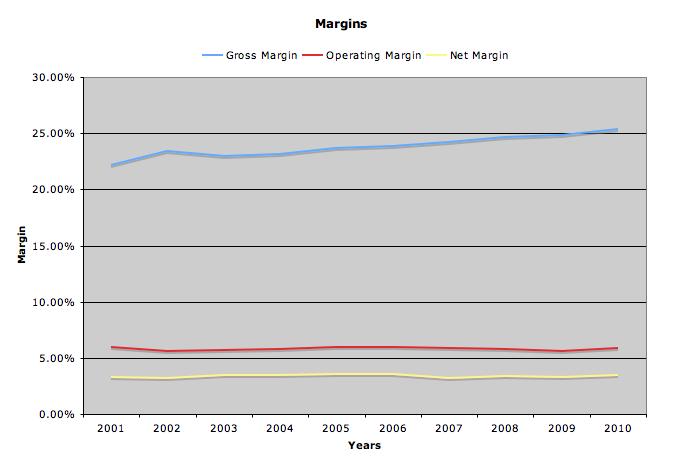

Revenue and Margins

| Years | Revenue (in millions) |

|---|---|

| 2001 | 193,295 |

| 2002 | 205,823 |

| 2003 | 231,577 |

| 2004 | 258,681 |

| 2005 | 288,132 |

| 2006 | 312.101 |

| 2007 | 348,650 |

| 2008 | 377,023 |

| 2009 | 404,374 |

| 2010 | 408,214 |

Revenue has grown by an average of 8.5% for the past 10 years

All margins have remained steady over the years, and gross margin has even grown slightly. Though low, these margins are normal for retail businesses.

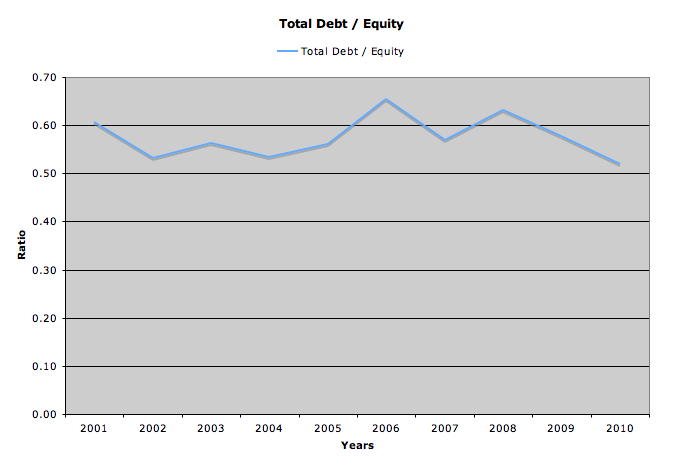

Balance Sheet

WMT’s debt is slightly higher than many other top quality dividend companies, but this should not be a problem. In October of this past year, they actually sold 5 billion dollars worth of bonds at some of the lowest yields ever. I believe the 30 year bond only paid about 5.1%. This was a great move by Walmart, taking advantage of yield hungry investors to lock in great interest rates. They can use this money to build up international operations, such as their recent attempt to acquire a majority stake in South Africa’s Massmart.

WMT has a current ratio of 0.8

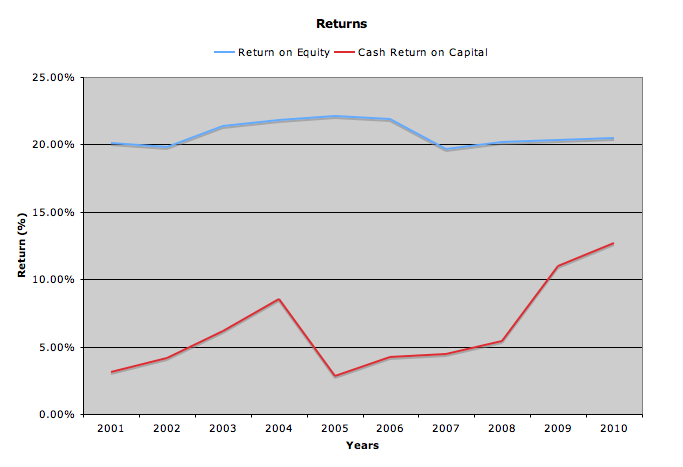

Returns

There has been a steady return on equity of about 20%. Cash return on total capital has grown over the years from a low of 3% in 2001 to a high of 12.71% in 2010.

Stock Price Valuations

current price –54.77

p/e (ttm) –14.80

p/e (forward) –13.52

p/cash flow –15.08

peg –1.36

dividend yield –2.21%

Conclusion

Walmart has all the makings of a dividend king. A long history of increasing dividends, a double-digit growth rate, and family wealth that is heavily invested in the company stock. They are aggressively pursuing international growth in many of the BRIC countries, though they did just close their Moscow office.

The yield is slightly lower than I look for, but their stellar dividend growth rate should compensate for this if you plan on holding for the long term.

Next week I’ll be analyzing Target, followed by Costco and then Family Dollar Stores. At the end of the month I’ll post my comparison chart.

10 Comments

I didn’t know that they closed their Mocow office, but then, that could always end up being a good thing in the end. If the environment isn’t conducive for high returns, then they should move on. I often wonder about corruption and palm greasing in Russia. Thoughts about that….anyone?

It seems from news stories and overall feeling that corruption is a serious problem in russia. The way they mix business, government, and police /military services can only lead to conflicts of interest, especially among top brass.

Recently, Russia was ranked 154 of 178 in Transparency Internationals Corruption Perception Index (CPI). In 2009 Ikea also halted expansion in Russia claiming “the unpredictable character of administrative procedures in some regions.” (full story here)